I saw this rather interesting video on youtube, and I thought it was particularly relevant to some of the recent discussions that have been going on about drawdowns.

In particular:

There you have it, spoken by a master - I also have been trying to argue the case, that to believe the max drawdown of any trading system has no relation to the max drawdown seen in the backtest, which can easily and forever be tweaked to bring it under control. I think he makes a very interesting point, if you are scared to have a 50% decline, maybe stocks are not for you, or you can keep some of it in cash. If you think you can control drawdowns with clever trading systems and market timing, then you are exactly the type of fool that lead us into the financial crisis, or the disaster of long term capital management. And the latter was run by the smartest fools in the world!

Oliver, there is a big difference between holding a stock like Berkshire Hathaway through thick and thin, and trading 20 micro-caps every week without worry about draw-downs. Holding the stock is investment in something worthwhile, trading the micro-caps is fooling yourself that you will double your money every year.

I tend to agree with the drawdown theory that you need to be able to take a 50 - 60% loss and stay in the game. But… you also need to understand what is driving your system and be convinced it will bounce back (e.g. valuation - possibly tied to dividends as opposed to momentum).

I would really like to see someone built a market-timing theory based on academic research pre-2008/09 as anyone can build a pretty-looking market-timing filter after an event to say they would not have invested in it. Or have a new designer only work with data 2003 and earlier without the benefit of changing the rules once he sees how it runs after that.

Any aggressive system with hi return potential has hi loss / DD potential. Yes. But…we should only stay invested if we believe 100% in the underlying return drivers of the system and that those factors will continue to be relevant in the future.

Buying Real estate after a 50% DD is a lot different from continuing to put money into a pattern trading 1 hour hold mean reversion system. But both can break. It just takes more for Real estate to never recover any value. Like a major war and gov’t overthrow and currency collapse. Those things have happened to major nations (Japan, Germany, the Ottoman Empire, etc). But more rare.

Munger and Buffett have a TON (maybe seven tons) of money. Half of a ton of money is still a TON of money. ‘Normal’ people who need those dollars to live…and / or are nearing retirement…will react much differently to DD’s. This is well documented. Read the research from DALBAR and others and you will see that individuals investing in market mutual funds lose 4-5% / yr. on average over many decades by ‘timing the market’ without any real system other than emotion. They change the amount invested in reaction to trailing year returns. However, almost all professional investors / asset allocators also do this. Research on how institutional investors behave shows the same thing. They tend to ‘chase performance’ in hedge funds and asset class allocations. Investing in what’s worked over trailing XX years and trimming allocations to what hasn’t. They are somewhat slower to adjust and chase, but they do. Even the pro’s.

Fifty years ago, if we lined up 50 aspiring fundamental managers, would we have picked Buffett and Munger out as the ones most likely to succeed? I doubt I would have. Why do we believe we could have? So, when their early years 50% DD’s came, would we have stayed? What is the track record of all the other ‘top fundamental managers’ who started at the same time as they did…in aggregate? What would doubling down on them have gotten us? It’s easy to find a ‘guru’ after they have a few decades of success. Very hard to find them before. These guys took highly concentrated positions…especially when building their return record. I wouldn’t have invested in them, most likely, if they walked in to talk to me with no track record or assets.

Doubling down during on a 50% DD is right until it’s wrong. When it’s wrong, people leap off tall buildings and bridges. And advisors have nervous breakdowns. I know people this happened to in the late 1980’s. That’s also what happened in 1929. That’s what would have happened in 2009 if the economy had fallen into the abyss. It happens when asset allocations to ‘risky assets’ get too large. But it happens over and over again.

Total DD can be controlled by asset allocation. Holding some money in cash and short-term holdings. Market timing systems can likely be part of that. I have posted too much on this elsewhere to add to it here. Market timing isn’t magic. Can’t protect against any sudden event out of blue, with no precursors. But, may keep you out of a recession that develops into a depression. And volatility clusters. The research on this is many, many years old and fairly compelling.

Equities and systems can underperform for multi-year (or multi-decade periods). The best time to invest in a system with real alpha is often during a DD. But how do we ever know a system has ‘real alpha?’ It’s hard even when we’re the developer. But where we’re not? It’s a leap of faith in the developer.

Hi-turnover systems are relying on the inherent ‘factor stability.’ Long-term ‘buy and hold’ are relying on continued investment by lots of people in the equity markets…and are relying on the P/E ratio staying constant and/or rising and continued GDP growth…and rising aggregate corporate earnings… Both can break down. But…the more rules a system has…and the higher its fixed annual costs, the more easily it will break.

This sound a little like the “endowment effect.” Some economists would say you should decide each Monday (or whenever you rebalance) whether you want a stock with no regard to whether you already own it or not. Of course, transaction costs and tax considerations enter into this a little bit. I don’t trade a lot of microcaps but losing 50% on a basket of small caps hurts about the same as losing 50% buying and holding S&P 500 stocks for me. Berkshire Hathaway is a little different in that it is actively invested albeit without a lot of turnover.

Good comments. Agree that we all tend to love past big winners ‘after the fact.’ Agree that losing 50% is losing 50%. But we do feel ‘worse’ when we are losing and the market and ‘everyone else’ is up. It’s more difficult for most investors to be contrarian to popular sentiment and wrong, then it is to be wrong together. And, while I like the theory of deciding on current investment / allocations only on future merit, my experience is that this will be a disaster if this process isn’t systematized and that system backtested thoroughly. Most people will end up chasing performance and lose a lot of money doing this. That’s what Dalbar and other research mentioned above also shows.

My MAC system works as follows, with a buy signal and a sell signal triggering shifts from investment in the markets to the safer, money-market-fund-like reserve.

A buy signal occurs when the 34-day exponential moving average (EMA) of the S&P 500 becomes greater than 1.001 times the 200-day EMA.

A sell signal occurs when the 40-day simple moving average (MA) of the S&P 500 crosses below the 200-day MA.

Historical investment results from this MAC system have been, on average, 2.4 times higher and less risky than a buy-and-hold investment in an S&P 500 index fund.

On paper, that seems like a sound method but I don’t think it would work in thew real world because it doesn’t account for structural changes in the financial/economic/market/etc. environment over time.

For example, a designer who works with data only up through 2003 will necessarily come up with models the underestimate the impact of large institutionally-driven block trading, underestimate the extent to which same is algorithmically driven and even more greatly underestimate the extent to which such algorithms are text as opposed to numbers based. Such a developer will also necessarily underestimate the impact of globalization and very drastically underestimate many correlations and inter-relationships. Such a designer would also be working with data from an environment in which the relationship between interest rates and economic activity and market prices was far more elastic than has been the case lately and may be the case going forward. (In fact, the impact of interest rates going forward is a massive unknown and one for which we have no data that can be used in modeling – we have data from past rising-rate environments, but not data that includes the possibility of lesser elasticities).

The science of model building cannot, in my opinion, ever be divorced from the art. And when it comes to timing, so far, the best model I’ve seen is the one that kept me heavily on the sidelines in the early 2000s and in 2008: look around, recognize that the market is going to hell in a handbasket, and get the heck out.

Tend to agree with you. But everyone defines ‘work’ differently. Some market timing systems, on a standalone basis will produce false signals and/or whipsaws and you will earn less using them. People’s opinions in these matters feel more like ‘religions.’ Some people are strongly in one camp or another. Some market timing signals will not call ‘big market drops’ and then will have you on the sidelines missing market bounces. I get that. But, in aggregate, I still use them. They give me a shot at missing the next great depression when, or if, it happens. A shot at not losing 50%. I’ll take that. Even if it costs me something in total AR%. But that’s me.

For me, simple moving average trend lines are the simplest and likely most robust form of avoiding many depression like events…if I could only pick one method. I have backtested several SMA rules for the entire US stock market history. They worked remarkably well. And, I just tested 36 parameter variations on your suggested rules. There is significant robustness with all of the rule permutations I tried (5 buy variations and 5-6 sell variations). All of the rules I attempted drastically reduced DD’s if used to trade the SPY ETF with monthly rebalance. Not one had a DD greater than 27%. Yes, they are not super tax efficient. But, trading with the trend is not a ‘fad.’

No. It may not achieve the best absolute returns. But, I don’t get why anyone would think that some systems with some timing rules don’t make sense as part of a book of systems?

I also tested your rules on weekly, biweekly, triweekly, monthly and quarterly rebalance. There was robustness. I have done many of these tests before.

So…for me. A basket of market timing rules belongs in many conservative portfolios, along with a buy and hold sleeve. And cash. And short-term bonds. But, that’s me.

“And when it comes to timing, so far, the best model I’ve seen is the one that kept me heavily on the sidelines in the early 2000s and in 2008: look around, recognize that the market is going to hell in a handbasket, and get the heck out.”

Yes, but to make that determination, you need to wait quite a bit “after the fact”. You never know if that model (today) will do what you are describing (keeping you out) or if it will turn out to be just a whipsaw that got yout out all right but lost you money because after the whipsaw it went up again.

There are many ways to control drawdowns besides market timing or clever trading systems. The oldest method in the world is simple diversification. With all due respect to Mr. Buffet and Mr Mungers longer term performance record, PRPFX has outperformed with less risk and less volatility since 1999: PerfCharts | Free Charts | StockCharts.com

(that’s as far back as the chart goes). And the simpler, original version of the Permanent Portfolio (equal parts US stocks, Long term treasuries, Gold, t-bills) did better with less risk over this timeframe. I think Berkshire takes the approach to maximize return. I prefer to maximize risk adjusted return.

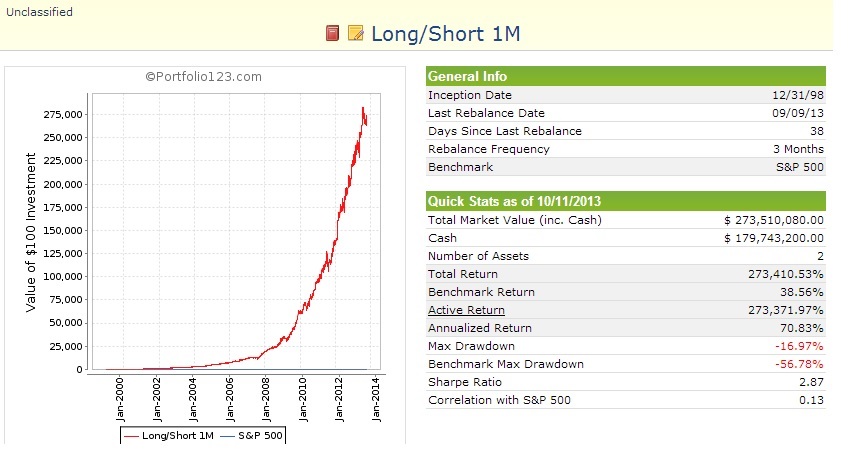

With trading systems there are many ways to diversify beyond simple asset classes. I don’t have Billions so I find a 50% drawdown completely unacceptable, so I will use all options available to me to reduce my risk, not just market timing. The Book option shows how effective diversification among non correlated strategies can be. Attached is an example with only 2 strategies (and I use a lot more strategies than that in live trading):

There has been too many opponents of market timing spouting how it doesn’t work out of sample, causes too many whipsaws, causes significant underperformance. And it can’t be relied on. I think those who are so against it are doing a disservice to the members who are new to trading stocks and P123.

My Grandfather talked me into putting 10% of my first engineering check I received after graduating from college into stocks and mutual funds in July 1968. He taught me to always use a stop loss, sell my losers, let my winners run, and DON’T GET ATTACHED TO ANY STOCK! He then talked me into selling everything in October 1969 as the market continued down to a 37% loss in 1970 due to the first oil embargo. He used a VERY simple market crossover. He had me reenter in August 1970. He recommended that I get out again in October 1973 as the market continued down to a 50+% loss in 1974 due to the second oil embargo. I picked up on using his timing approach and was able to avoid about 10% of the market’s loss in 1982. The only big loss I was not able to avoid was the 30+% loss on Black Monday in October 1987 although many of my stocks were sold that day due to my stop loss. My stop losses saved me a bundle on 9/11, and market timing saved over ½ of my potential losses in 2001-2002, and 2007-2008. Yes, there have been a few times that I have been whipsawed and missed a few % during a market rise, but never more than 4%.

Now, before anyone else claims that market timing doesn’t work, I want you to justify it with actual information and/or data showing a timing system that has failed to protect capital during major drawdowns, and had many whipsaws that caused significant underperformance. Otherwise allow those of us that have been using timing successfully over and over help the other members avoid major losses, sleep much better at night, and reap the benefits of investing in the stock market.

I believe a professional investor like you can do that. As far as research on the retail investor (like me) I think it might show that we get it backwards. We go out at the bottom and buy at the top, I think. I can confirm a strong urge to to that at times. Although, I was at least smart enough to put some money to work near the bottom of 2008. That aside, P123 does help me not to make dumb trades based on Kudlow’s mood (or Cramer’s rants or Fast Money’s really fast changes for that matter).

Indeed, it can be argued in this zero sum game, that retail investors are why the professional investors make money. I appreciate that you are one of the professions helping the retail investor.

I used to use a crossover of the 50 day and 200 day SMA. From my reading of long term studies it does seem to help some (the actual study was close over 200 day moving average by some percentage). However, the long term studies did not impress me that much and I stopped.

I do use market timing but for me (so far) it is in the hopes of not getting killed rather than increasing my absolute returns.

In late 2008 I tested a variety of moving averages and moving average cross overs against a number of index based mutual funds, going back 20 years. In case that wasn’t enough I did testing on the DOW back to 1926 or so, the Nikkei bear market (from the peak), and the Nasdaq bull market (to the peak). What I found was that generally market timing with moving averages improves risk adjusted returns. There were some exceptions but they were very few compared to the number of tests. Sometimes it improves absolute returns. The difference is important. In my opinion the goal of market timing is to improve risk adjusted returns, not necessarily to improve absolute returns..

Oliver, I believe a timing method that I heard about from you, to be long when bench > sma(50) or bench > sma(200) was developed before the 2008 crisis. In any case it has done well since.

Both sides of this argument have some merits. Clearly in hindsight timing methods that are over optimized and curve fitted can be developed, and such approaches are likely to be worse than useless going forward. This does not mean that all timing is non-robust and useless. Simple moving averages have been proven many times over. I have not seen as much data supporting timing based on the VIX and earnings, but I’ve seen enough evidence for me to consider such approaches for at least part of my portfolio.

Good stuff. Have you tested how this SMA(200), or 10 month SMA, timing model does with a high CAGR model like your R2G ports? It does seem that the hedging you often recommend might do better than getting completely out of the market.

Don - I agree with you in principle but I should point out that PRPFX didn’t really escape the drawdown of 20089 and hasn’t gone anywhere in the last three years. I think this is a reflection of the high correlation between asset classes which may be here to stay, or at least for a very long time.

Long/short is great if you have a good short system that will hold up. A good pullback system combined with a value system may also give good results. Or maybe not.

Not necessarily. When I say look around, I don’t necessarily mean look around at stock prices and indicators. I also mean look at the world in general; the fundamental factors that drive the market. The tendency among people who work this way is to pull back too far before the market starts going to you-know-where and give up a lot, if not all, of the last upside surge. It’s often the same on the other side, a tendency to be early rather than late. and the difference between a correction (nothing ever moves in a straight line) and a serious problem usually involves the presence or absence of some sort of “excess” in the system. Fundamental, economic, etc. factors can go a long way toward helping us distinguish an actionable state of affairs vs. a likely whiplash.

I think the comments about 50% drawdown being unacceptable for non wealthy are quite telling.

Is that surely not the point? If you need to “pay your bills” or whatever, then you shouldn’t be doing it with funds invested in the stock market?

A drawdown is not quite the same as plainly losing money - it means your equity portfolio will fluctuate, and at sometime it may show a top to bottom decline that is a high percentage, but it may well be more than you started with in the first place, and indeed, markets will eventually rebound, unless you are plain gambling.

Also, I want to make it clear I am not anti-market timing, but I think it is important for people to realise it has severe limitations. There is a very limited amount of periods we can test signals on, and really far too many degrees of freedom. If you have the discipline to stick to a very simple approach it can be effective. As Don rightly pointed out, I did post a system back in 2007, and it would have cut your potentially 50%+ drawdown to 25% over the period.

However, the key point is risk cannot be asssed by looking at historical performance alone. We might have another 1987 style crash that comes out of “nowhere”. If you really want to limit drawdowns keep some money in cash, this is the only way to guarentee it (not forsaking the risk of hyperinflation of course!)