I consider the S&P500 overvalued on several metrics. Not going to time off valuation but philosophicaleconomics did a nice piece on adjusted-CAPE.

EPS trend is not looking good by the P123 graphs. Energy is obvious issue, but so was tech in 2001 and financials in 2008.

The equity risk premium favours equities and the equity market has supportive breadth.

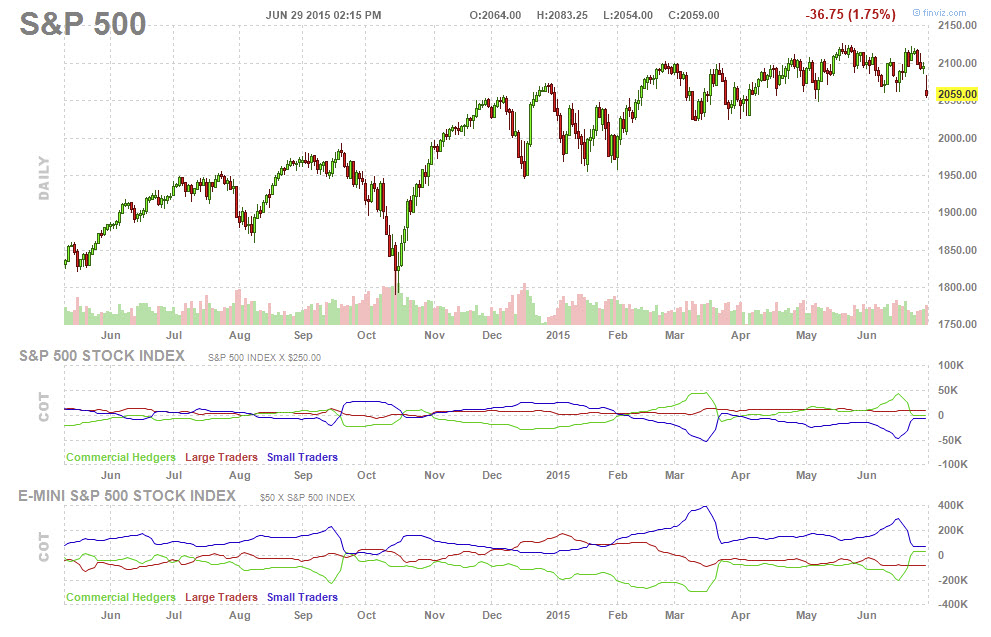

The fact that SPY:IEF is flat for a while means we are struggling in equities, yet VIX < 14. With high PE, this ratio of PE/VIX shows complacency.

For the next month I am long equities but have been buying a few Sep SPY puts with portion of profits on good days.

What are the degrees of freedom for policy here?

Fed Funds - same or up 25bps. June? Sept? Reported unemployment says hike already. Participation adjusted says hold, but also that policy measures are working very slowly. Increase in rates will strengthen USD, hurting exporters over domestics but will also spur lower inflation. I expect low rates for years.

Long rates - the world could notice that they get more coupon and a great FX trend, buy up US bonds in 5/10/30 and flatten the yield curve, which would increase the equity risk premium and might be the trigger for an equity melt up as everyone would be more fearful of interest rate hikes then.

Black Swans

Global slowdown - Fed will start QE4 and excess liquidity sloshes into financial assets…again.

Mergers - expect mega mergers as CEOs buy growth. This may lift multiples in market supporting rise.

ISIS invades Saudi Arabia - oil doubles, global recession, US led coalition into region.

Iran gets sanctions lifted - releases lots of stored oil, price falls hard, US consumer benefits

Bank of Japan - goes full retard on weakening yen and buying stocks but yen weakness runs away from it and confidence in central bankers questioned