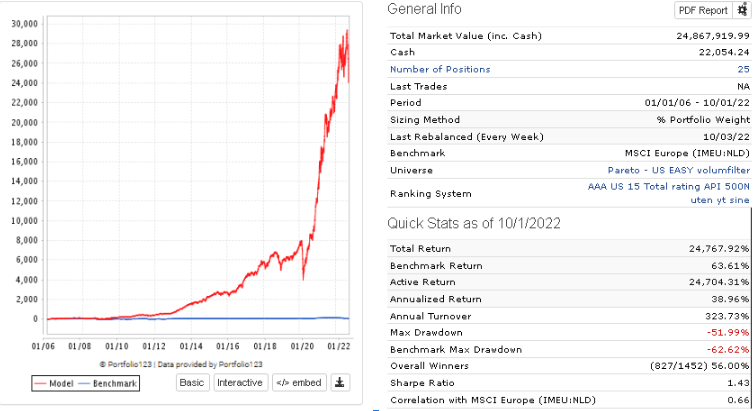

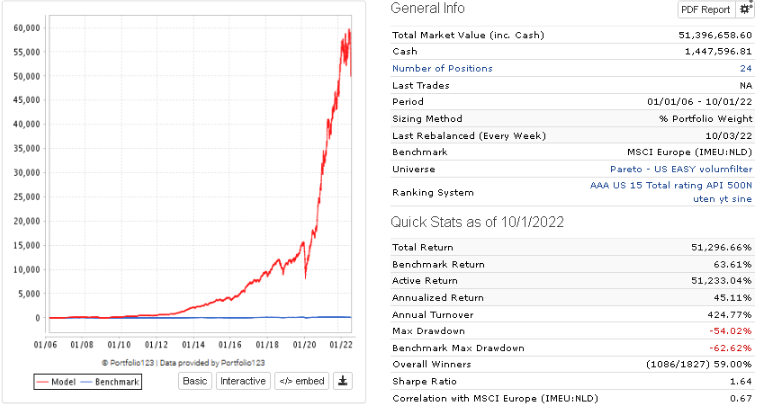

Here is a site and programmer/trader that interests me: https://etfoptimize.com

I think Chris has alway had a point in the forum. I take his comments/suggestions seriously.

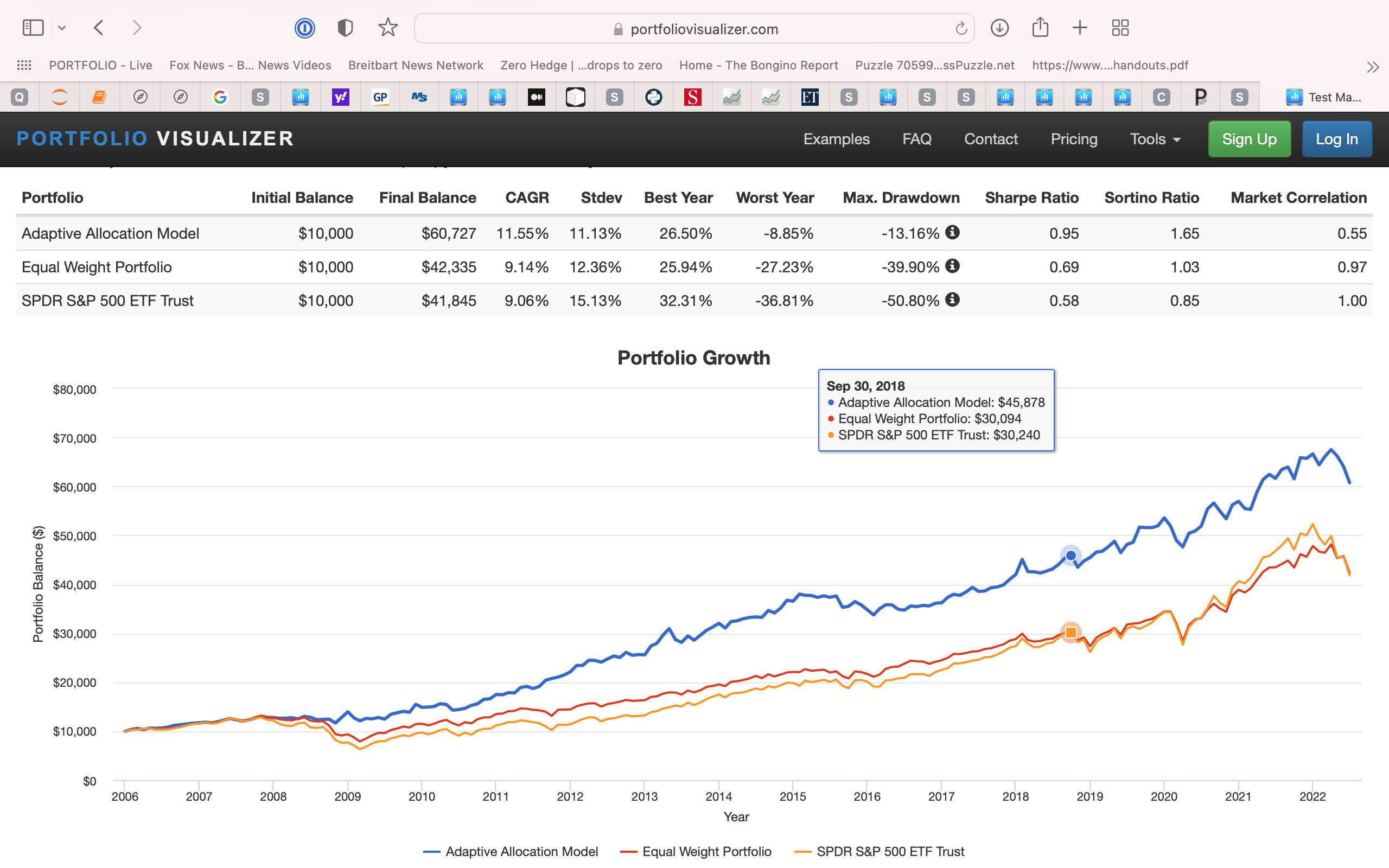

But leave that aside for a moment. Here is a site that has a pretty good and consistent following. From a business perspective it might be interesting: https://www.portfoliovisualizer.com

The problem with Portfolio Visualizer (and where dramatic improvements can be made) is that is does not have much in the way of indicators (technical or otherwise). What it has is rudimentary.

My only point for P123 is that it would be relatively trivial to dramatically improve on Portfolio Visualizer’s site if there happens to be a business case for it. The computing power required is not large compared to what P123 does now. Using the ML algorithms above would be just one way to make a dramatic improvement and it is clearly not computer-resource intensive.

We don’t really know whether P123 employs a ML specialist anymore (we never hear from her in the forum if she is still there). Or whether P123 continues to focus resources on AI programs recognizing classic trading patterns (a pretty resource intensive and complex coding endeavor that may not be possible for P123 in the end).

P123 bought some GPU’s (or pays for access) in an attempt to complete this maybe? How many patterns can it recognize? What is its accuracy (precision, recall)? Can it learn and recognize new patterns? How much time have you spent? Are you done with the coding?

Personally, I would rather use the FED data with AI models and it is already in tabular form on P123’s computers. [color=firebrick]I think that would be a huge improvement over what Portfolio Visualizer does and everyone would recognize it. I think some people at Portfolio Visualizer would be signing up at P123.[/color]

P123 can debate Chris, Andreas and others about the value of technical indicators. P123 will be right on many counts. Me, I would just ask if there is a market.

For now, if you want to do ML you need to know some Python. The above program is one I have found helpful. I am absolutely sure there are better programs. Working to prove that my program is not that good would not address whether there is a market for good, professional programs.

Many find P123’s API helpful. We do not know what everyone is doing with the API but it suggests they might be using some algorithms that P123 does not provide now. There may or may not be a business case for P123 to provide some of those algorithms themselves (without a lot of debate from P123 about what P123 think they should be doing with outside programs).

P123 could consider whether there is a business case for provide programs for people focused on doing other things with P123’s API or for those not actively running Python programs now.

P123 is free to focus its resources wherever it wants without paying attention to Chris or Andreas or even Yuval really. Unless, Yuval thinks technical trading patterns is the one technical indicator worth pursuing.

Me I have no problem with P123 providing technical trading patterns. I just wonder if that offers the best bang-for-the-buck. If that is the best use of resources.

Just one idea if P123 actually takes feature suggestions anymore. Or if P123 welcomes any discussion of any ongoing development of AI capabilities.