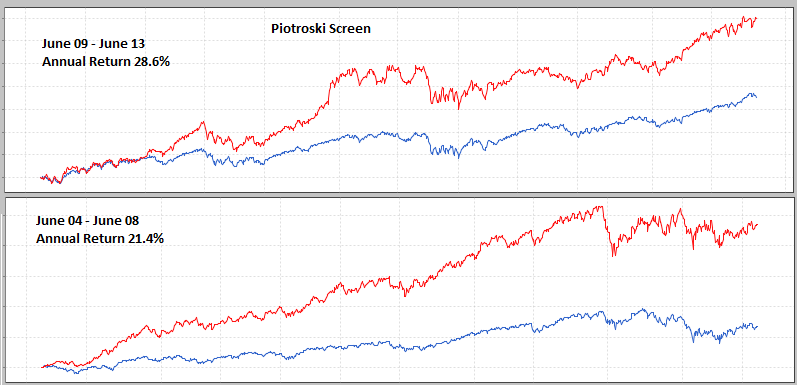

I seldom wish to comment about R2G models in Portfolio123.com as I respect all the designers in this forum.

I stand by my position that my investment return gave me much better return by using my portfolio123.com models vs. without them.

Ask yourself this question, if you do not have any R2G models or your own models to follow, what other ways could you do ?

I can think of a few possibilities to illustrate the points :

-

Search for all the stocks in DOW30 and look for stocks that have SMA(5) > SMA(20) and stay with them until SMA(5) < SMA(20) happen before you sell out. Likely you can achieve the objectives of high liquidity and low slippage. But my questino is what will be your buy price ? exactly at the price that the moving averages crose each other or higher price than that since the crosss over happened three to four days ago and ended up your slippage is much higher percent ? (unless you check for the MA cross over everyday)

-

Follow the dogs of the DOW by buying the few stocks in the DOW that pay the highest dividend yields exceeding say 3-3.5% payout per year. Do nothing after buying it and do a yearly rebalancing by reviewing the dividend pay out again. How to calculate slippage in this case ? I really don’t know.

-

Trade the SPX500 or DIA or Rusell2000 3X ETF with SMA(5) > SMA(20) and sell when SMA(5) < SMA(20). in this case what will be the slippage ? I don’t know because it depends on how you measure the slippage (at reference to which point, daily check, weekly check or hourly check) ?

My opinion is that any R2G models or our own portfolio123 models are mathematical models. They have to be based on price quoted either at the end of the day, may be Friday closing price since most of us only have time over the weekend to do some of these re-balancing work. So some form of slippage is build into our way of buying and selling.

So what’s the bottom line ? My conclusion is that whether a system that we follow enable us to make real profit realistically and the model(s) we follow behave in a very predictable way. If the answers to above is “YES”, the question then become whether you can accept the risk of following it since to a R2G subscriber, it is black box trading with the only known downside being the max drawdown in the last 10 - 12 years and how the model behave during 2002, 2008, 2011 in which these are very volatile years for stocks. It will be good we revisit this topic two to three years later after the R2G models go through a serious down draft in stock market and see how many R2G models survive the acid test.

In addition, to follow a R2G model, the best approach is still to be able to follow market price movement in the first half hour of trading on Monday morning and close the trades within the first hour of Monday to try to match the prices in our model. Will we suffer slippage, we definitely will (regardless of which method we follow, even the mothods above by not using portfolio123 ). My own measurement of whether a model works well or not is to calculate the average return%/avg days of per stock holding.

Eg.

Case A

avg gain% is 9% and avg holding is 30 days, ratio is 0.30

Case B

avg gain% is 6% and avg holding is 20 days, ratio is 0.30

So, in which case we need to pay more attention to slippage ? I guess it is very clear case B will have more issues with slippage due to shorter holding period and more frequent trading.

If we have a

case C (let say a micro-cap port with slippage is 1% on buy side and 1% on sell side)

avg gain % is 12% and avg holding is 40 days, ratio is 0.30

comprehending the slippage it will becaome :

avg gain% is 10% and avg holding is 40 days, ratio is 0.25

question is are you satisfied with ratio of 0.25 using this strategy ? If the answer is yes, then it is ok to allocate money to it.

I write all of this is not to defend my R2G models but to defend the great job from Marco and his team for making R2G models available in Portfolio123.com. please bear in mind portfolio123.com need to make profit as a company as well in addition to offering this great services to all of us.

In addition, everyone of us have different risk tolerance and different market temperament. This differences in temperament in us will also create diverse of % slippage in our own trading to mimic the model performance.

So here, I rest my case on focusing/emphasising so much on Liquidity and slippage. Please do some calculation first and compare them with other strategies that I tabled out above or other investing strategies that you have and you will be smart enough to figure out what make sense to suit your own temperament on stock trading and whether to follow R2G models or to leave them alone.

Wuu Yean